This is part one of a three part series on SAP HANA.

Many years ago, SAP’s founders had the dream of implementing accounting and finances in real-time. They believed this could revolutionize business, making it possible for enterprises to have a clear picture of their financial positions at all time, enabling companies to make better decisions. Ultimately, this vision grew to include business processes across the enterprise, supporting real-time integration across all business processes in the enterprise. Over the years, SAP and other vendors have not always accomplished this level of real-time integration, but the days of batch processing of invoices, receipts, inventory updates, and other crucial enterprise information are largely behind us.

Except in business intelligence. Most enterprises today extract data periodically from their operational systems, transform that data into unified units and schema, cleanse the data of errors and gaps, aggregate the data to support faster queries, and then deploy that data into the enterprise data warehouse for reporting and analytics use. This process generally introduces a lag between when data are entered into the operational system, and when that same data are available in the data warehouse. This lag can be as short as a few minutes, or as long as a month, but is rarely less than an hour. Many enterprises “refresh” their data warehouse nightly (although when is “nightly” in a global enterprise?) or even weekly. One CRM system I used recently had a caveat on its reports, stating that “the data in this report may be 24 hours out of date.” In other words, on the last day of the quarter, a sales manager could not use the system’s reporting capabilities to determine if she had made her quota or still needed to make some more calls. For some applications, this lag time is unavoidable, but eliminating this gap between action and insight should be a goal of every IT organization.

For many enterprise topics, new ideas come from the consumer world – this trend is known as “the consumerization of IT” (or #CoIT, to insiders on Twitter). Consumer-facing companies (like Apple and Facebook) hear more clearly from their users and customers than Enterprise Software and Solutions companies (#EnSW on Twitter), and so they are often the source of innovation in the IT space. CoIT gives us many ideas about user experience (iPad!), social capabilities (Facebook!), mobility (iPad!), and scaling to massive data volumes (Facebook!). However, the consumer world does not offer us many good examples of real-time integration of operational and analytical data.

Into this critical need – powerful analytics on current data with real-time response – stepped SAP recently with SAP HANA. SAP aimed to bring the same real-time advantages to analytics that they brought to transactions. HANA is an extremely ambitious undertaking for SAP, which is not known for its leadership in the worlds of databases or analytics.

Over the years, SAP has offered its own database (SAP DB), which did not have a great deal of success in the market despite the obvious pricing advantages in comparison to commercial database products. Most notably, Oracle has been adopted by most large SAP customers, both for their operational databases and their data warehouses; Oracle has focused on the needs of large customers, and has achieved scalability, stability, and operational reliability not generally available from other commercial databases. Open Source databases have lagged far behind in these areas.

Additionally, SAP has offered first reporting and then generalized business intelligence solutions of its own (e.g., SAP BW), but these products have achieved only limited success, and that only in the SAP installed base. SAP BW has about 13,000 customers, but many of these customers use other analytical products alongside their SAP BW environments.

Recent years have seen SAP begin to make some serious moves to improve their position in the database and business intelligence spaces, specifically through the acquisition of Business Objects and Sybase. SAP has vaulted to a real leadership position in the BI world with the combination of its BW and “BOBJ” products, although it is still a distant #5 in the database market according to IDC.

If SAP could offer a discontinuous breakthrough, a game-changing technology, it might be able to capture a much larger share of this lucrative market, bringing some real benefits to the SAP shareholders and employees. Further, with Oracle's large share of the databases in SAP environments, a large increase in SAP’s share of this market would likely most hurt Oracle, SAP’s largest competitor in the applications business, reducing Oracle’s ability to fund its competing applications products through database profits, while simultaneously reducing Oracle’s insight into applications customers’ needs. Finally, if SAP could come up with a technology that provided real, new benefits to its customers, such as dramatic reductions in TCO, dramatic improvements in performance, or unification of the operational and analytical data stores for real-time data analysis, then SAP would be providing its customers with the kinds of benefits that could bring new levels of performance to their enterprises. This is precisely what SAP has set out to do with SAP HANA.

SAP HANA has no entered ramp-up, where SAP will take it from the first handful (or, technically, two handfuls) of customers up to several dozen, and then on to hundreds and thousands. Notably, SAP is using HANA internally, to speed insight for top management. At this point, HANA is primarily being used as a high-performance data store for BW, but stand-alone applications (such as “CO-PA Accelerator”) are not far behind, and eventually SAP plans to run their full suite of applications on HANA. Yes, that would mean a great potential savings for customers, and a significant reduction in business for Oracle, but this is years away from reality. In the meantime, SAP HANA looms as a potential boon to SAP shareholders, employees, customers, and partners.

The next blog in this series will discuss how to tell if SAP HANA is right for your organization – or for you.

Thanks to Mike Fauscette and IDC for providing market share data for this blog.

Please note: as of the time this blog was written, SAP is a current client of the author's.

SAP HANA has garnered a great deal of attention in recent weeks and months. For an overview of the technology and its potential, please check my recent blog on the subject, "The real (potential) impact of SAP HANA."

Since that blog was written, there has been a great deal of news in the SAP HANA world, and the surrounding cosmos as well. Rather than write another long blog on this topic, here is a list of some highlights:

The pricing of SAP HANA is getting clearer. A low end (128GB to 256GB RAM) SAP HANA appliance could start at around $80K-$100K for the hardware. A few sources inside and outside the company (not under NDA) also indicated to me that the price of SAP HANA software is around $120K at the low end, stretching up to $1M to $2M at the high end. SAP says the pricing is not discountable, but early customers have told me that (at least for them), everything is negotiable. This puts the entry-level SAP HANA pricing at around $250K plus services. A pilot project could be done for less than $300K, with potential for very large business benefits. How hard is it to find a business analytics problem that is worth $300K if it can be completed 10x faster? For many businesses, there is no shortage of such analytics problems, and in some cases SAP HANA will actually perform 100x faster - or even better.

Pricing for higher end SAP HANA boxes is not as clear. If your data can fit into 1TB of RAM, then these single-system boxes should be OK for you. But how will you know if your data can fit into that memory size? It seems (and I would welcome a knowledgeable person's correction on this if inaccurate) that SAP HANA can't be used when data can't fit entirely into one system's memory, which currently tops out at 2TB (and at much higher pricing - an additional $250K or so, from those few vendors offering that high-end configuration).

How much data can fit on any SAP HANA configuration? From discussions with a number of current SAP HANA users, this is not always clear, and SAP has some work to do to deliver good sizing tools. On average, users I spoke with report compression ratios of between 4 and 10 times for data - that is, if the data would take up 400GB in an ASCII file, the same data with HANA's columnar compression would take between 40GB and 100GB in SAP HANA (your mileage may vary). Of course, the operating system and other software needs some memory to run, but this size of data should fit fine onto the smallest SAP HANA appliances. In a disk-resident database, you might need dramatically more disk space for such a data warehouse, since space will not be used efficiently (sparse data) and since the indices may take a significant amount of space - even more than the data sometimes!

How about this for a sizing tool - load all your data on a removable hard drive (ENCRYPTED!!!), and bring it to IBM, HP, Cisco, Fujitsu, Dell, and anyone else offering a SAP HANA appliance. Have them load it up for you on their hardware, and test out your queries. If everything is as simple as some customers and integrators have been telling me (which is pretty close to how simple SAP has been saying it will be), then the hardware partners should be willing to do a pilot like this for free. You'll know exactly how much hardware you'll need, and you'll have a very good idea of its performance!

As a killer new application, SAP HANA will be certified in November for running SAP BW. All BW reports, extractors, etc., should all run without changes (except MUCH FASTER) on SAP HANA after this release. Let's face it - the overwhelming majority of SAP BW data warehouses are running on Oracle databases. If you have an Oracle database license priced in the range of $800K (and many medium-sized data warehouses are on such licenses), with a 25% annual maintenance fee, you are talking about $200K per year just for the database maintenance. If you could migrate that database over to SAP HANA, you might find that you paid for it in the first year by dropping your Oracle maintenance, and at the same time you may be delivering ten times more users or ten times faster results on reports and analyses. It wouldn't be hard to imagine many Oracle databases being converted over to SAP HANA in the coming year - especially those running under SAP BW (and Business Objects soon too!).

SAP recently also discussed several analytical applications that will be made available on SAP HANA. These are interesting, but not where the short-term value will be for most customers - this will be SAP BW or Business Objects running on SAP HANA, and ultimately the rest of the SAP Business Suite running on SAP HANA. Or Sybase, for that matter.

Oracle may be feeling some heat from SAP HANA - Oracle just introduced a low end database appliance offering, with hardware and software bundled for between $100K and $300K. While it is unlikely that this appliance would be able to deliver comparable performance to SAP HANA for those applications most suited to HANA's current capabilities, this appliance would have broader application - for example, being currently suited to running production transactional applications such as SAP.

At the high end, a SAP HANA appliance might cost on the order of $1M for hardware and $1M for software. An Oracle Exalogic data warehouse solution might cost 10x that number, delivering slower performance, consuming a lot more energy, and taking a lot more space.

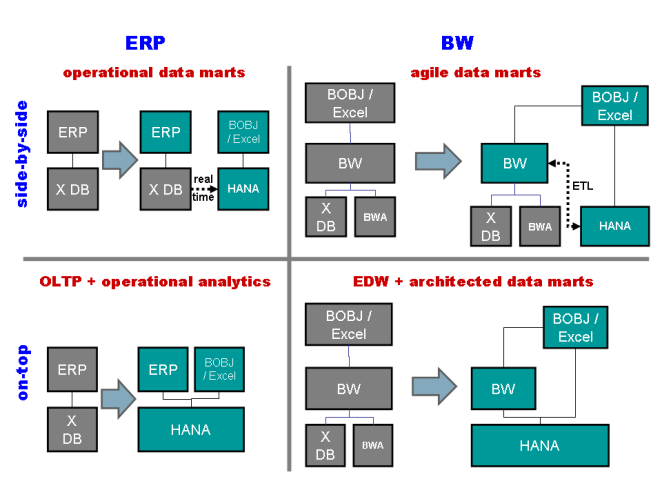

SAP has expanded the mechanisms for loading SAP HANA. You can now use log-based replication (replaying the logs on another database to copy it), and trigger-based replication (having a system notify SAP HANA when data is changed), as well as the previously available ETL-based replication (using BW extractors or other technology to copy data out in bulk/batch). The trigger-based replication mechanism is particularly interesting, because it updates the "data warehouse" (can you even call it that anymore with technology like this?!?) continuously, in near real-time. In addition, the trigger-based replication approach allows for consolidating data from several databases quickly and easily into a single data warehouse. If you have one database for your CRM system and another for your financials, both databases can propagate their updates into a single SAP HANA system for consolidated reporting and analytics. Trigger-based replication supports many-sources-to-many-targets replication.

Business Objects metadata integration with SAP HANA metadata was not announced at SAP TechEd in Las Vegas, but perhaps will be available soon. Business Objects Explorer can run today on top of SAP HANA, which gives some level of integration that will benefit many SAP customers running SAP Business Objects. The more integration at the metadata level, however, the more appealing SAP HANA will become to Business Objects customers not running SAP systems.

Conclusions:

SAP HANA is getting to the point where any customer running SAP analytics (especially SAP NetWeaver Business Warehouse aka BW) should be starting or at least planning an evaluation.

SAP HANA will make its biggest impact - for customers - initially as an "accelerator" for SAP BW.

SAP HANA may pay for itself in reduced database maintenance payments ...

... thus its biggest impact - for vendors - in creating pricing pressure on Oracle RDBMS for data warehouse instances.

We may be still a long way from seeing SAP HANA replace Oracle, IBM DB2, or Microsoft SQL Server as the transactional data manager for SAP Business Suite.

I worked for SAP for six years, including the period when SAP originally acquired the technology at the heart of HANA. SAP is a client as of the time of this writing.

Much has been written about SAP HANA. The technology has been variously described as "transformative" and "wacko." Well, which is it?

Disclosures I have a few disclosures to make before I continue my analysis and comments on Hana:

I worked at SAP for six years, as well as eight years at Oracle (plus also at Ingres before that).

I was at SAP when the technology underlying HANA was acquired, though I am referring to and using no trade secrets or proprietary information in preparing this analysis.

I attended this year's SAPPHIRE conference in Orlando, and SAP paid for my airfare and hotel.

Relational Databases Relational databases have dominated the commercial information processing world for twenty years or more. There are many good reasons for this success.

Relational databases are suitable for a broad range of applications.

Relational databases can enable access to data relatively efficiently even if the query was not initially envisioned when the database was designed.

Today's relational databases are economical, available on a broad range of hardware and operating systems, generally compatible across vendors, performant for many queries, scalable to fairly large data volumes without resorting to partitioning, suitable for partitioning when larger scale is required, based on open standards, mature, and stable.

There are a large number of developers, administrators, designers, and an ecosystem of service providers who are very knowledgeable about today's popular relational databases, and who are available at economic rates of pay.

NoSQL, Columnar, and In-Memeory Trend There is an emerging trend towards databases that are designed to solve specific problems. While relational databases are good for solving many problems, it is easy to conceive of specific problems that are not well-solved by general-purpose databases. Relational databases are well-suited to handling structured data where the schema does not change, where text processing is not an important requirement, where data is measured in gigabytes rather than petabytes, where geographical or time-series (e.g., stream) processing is not required, and where the server does not need to support transactional and decision-support queries simultaneously.

Some problems do not fit those criteria. The data set is such that the schema varies from record to record, or over time. Text, image, "blob," or geographical data may be a dominant data type. More and more frequently, applications manage "big data," or huge volumes of data from millions of users or sensors. Some applications require simultaneous access to data for transactional updates as well as for aggregation in decision-support queries. For all of these cases, advanced architects and developers are looking at specialized data stores and data processing systems such as Hadoop, Cassandra, MongoDB, and others. These domain-specific data stores are known as "NoSQL" databases.

There is some controversy over whether NoSQL means "no SQL" or "Not Only SQL." Regardless, those non-relational stores such as Hadoop, are growing in popularity, but are not really a replacement for relational data stores. A key property of most commercial relational databases is their compliance with a principle called "ACID," which essentially guarantees that database transactions occur in a reliable way. Many NoSQL databases use techniques like "eventual consistency" to improve performance at the cost of inconsistent data - a sacrifice that is unsuitable for most business applications. After all, if you deposit money in a bank account, you want it to be available for withdrawal right away, not "eventually."

Another trend in the database world is towards new methods of storing data, without eliminating the ACID properties that business applications need, and without sacrificing the SQL language that is so well-known and widely supported. Two specific approaches are quite popular these days - columnar storage and in-memory databases.

Column stores, such as HP's Vertica or SAP Sybase IQ, store data by column. By contrast, traditional SQL databases store data as rows. The benefit of storing data as rows is that it is often the fastest way to look up a single value, such as salary, given a key value like the employee ID.

Columnar databases group data by column. Within a column, generally speaking, all the data is of the same type. A columnar store, therefore, stores data of a single type all together, which can give advantages such as the possibility for significant compression. Good compression can lead to reduced disk space requirements, memory requirements, and access times.

In-memory databases take advantage of two hardware trends: a significant reduction in the cost of RAM, and a significant increase in the amount of addressable memory in today's computers. It is possible, and economically feasible, to put an entire database in memory, for fast data management and query. Using columnar or other compression approaches, even larger data sets can be loaded entirely into main memory. With high-speed access to memory-resident data, more users can be supported on a single machine. Also, with an in-memory database, both transactional and decision-support queries can be supported on a single machine, meaning that there can be zero latency between data appearing in the system, and that data being available to decision-support applications; in a traditional set-up where data resides in the operational store, and then is extracted into a data warehouse for reporting and analysis, there is always a lag between data capture and its availability for data analysis.

SAP HANA Several years ago, SAP acquired Transactions In Memory, a company that had developed an in-memory database. Over the years since, at virtually each annual SAPPHIRE conference, SAP has discussed how this in-memory technology would revolutionize business computing, but I personally found the explanations to be somewhat short on convincing details.

Even the name, HANA, has changed in meaning over the years. Initially, the name stood for "Hasso's New Architecture" (and a beautiful vacation spot in Maui, Hawaii) and referred only to the software. Today, HANA stands for High-Performance Analytical Appliance, and refers to the software and the hardware appliance on which it is shipped. In addition, HANA has evolved from a data warehousing database into a more general purpose platform.

SAP HANA does manage data in memory, for nearly incredible performance in some applications, but it also manages to persist that data on disk, making it suitable for analytical applications and transactional applications - simultaneously. But HANA's capabilities do not end there, and that may be the key to HANA's long-term value.

In the short-term, it seems that SAP still struggles to generate references for HANA, other than in a narrow set of custom data-warehouse-type analytics. That may obscure where HANA can really deliver its first market successes.

When HANA is generally available, it is expected to include both SQL and MDX interfaces, meaning that it can be easily dropped into Business Objects environments to dramatically improve performance. Some Business Objects analyses, whether in the Business Objects client or in Excel, can achieve orders of magnitude of performance improvement, with very little effort. Imagine reports that used to take a minute to run now running instantaneously. Imagine the satisfaction of your BOBJ user community if all or most of their reports and analysis ran instantaneously. Line-of-business users will pay for this capability, and that will open the door for SAP HANA in Business Objects accounts. After HANA gets in the door, I'm sure the CIO will find tons of additional uses for it. This is huge, and will generate truckloads of money for SAP, while also making customers super-satisfied.

And think of what SAP HANA means for competitive comparisons with Oracle, SAP's maximum enemy. Larry wants to sell you Exalogic and Exadata machines, costing millions; Hasso wants to sell you a simple, low-end, commodity device delivering the same benefits. If I were SAP, I'd have sales reps with HANA software installed on their laptops, demonstrating it at every customer interaction, and comparing it (favorably) with Oracle Exadata, and suggesting that customers demand that Oracle sales reps bring in an Exadata box on their next sales call - and not to bother showing up without one. Larry wants to sell you a cloud in a box; SAP will sell you apps on the cloud, or analytics in a box for hundreds or a thousand times lower cost than Oracle's solution.

The longer term benefits of HANA will require new software to be written - software that takes advantage of objects managed in main memory, and with logic pushed down into the HANA layer. I'll post more on this potential in the future, but just think of what instantaneous processing of enormous data sets will mean to business - continuous supply chain optimization, real-time pricing, automated and excellent customer service, and much more.

Summary In the long run, SAP HANA may indeed revolutionize enterprise business applications, but that remains to be seen. Right now, SAP HANA should be capable of creating substantial customer benefits - and generating a very large revenue stream to SAP.

I'm a huge fan of primary research, especially when it is paired up with great analysis. Some Enterprise Software and Solutions (#EnSW on twitter) analysts base too much of their commentary and advice on what they read in the news, see at user conferences, and hear from other analysts.

Computer Economics is an #EnSW analysis firm with a difference. Frank Scavo and the folks at Computer Economics do great research - quantitative and qualitative - on the #EnSW world. If you are an IT executive, or an #EnSW vendor, you owe it to yourself and your enterprise to check out their research.

The latest published research from Computer Economics is a study called "Go-Forward Strategies for Oracle Application Customers." In the spirit of full disclosure, I should mention the following, and you should bear these facts in mind as you consider my comments:

I have been in the #EnSW world for around 25 years now, including long stints in executive product roles at Oracle and SAP.

My company, C3, may someday be competing with Oracle (and other #EnSW vendors).

Computer Economics provided me with a copy of this $995 report at no cost for my review.

Here are some key findings from the report, followed by some of my thoughts about the results:

Finding: Dissatisfaction with the cost and benefits of support runs high across the Oracle Applications customer base, with 42% of respondents reporting dissatisfaction with the quality of Oracle support, and 58% reporting dissatisfaction with the cost of Oracle support.

My thoughts: That is a very surprising result, showing an astonishingly high level of dissatisfaction!

Finding: Customers generally expect Oracle to grow as a share of their IT spending, despite their level of satisfaction.

My thoughts: There are a number of obvious reasons for this result, including vendor consolidation, customer expectations of growth in their business coming out of this continued weak economy, and the difficulty of moving from one application product set to another.

Finding: Third party maintenance and support is attractive to a substantial fraction of Oracle Applications customers.

My thoughts: A far smaller percentage of Oracle Applications customers are considering third party maintenance and support as compared to the fraction who are dissatisfied with support quality and price. It is not clear to me that any third party can really deliver bug fixes, patches, and legislative and regulatory updates. Nonetheless, #EnSW vendors are increasingly dependent on maintenance and support revenue, and thus they are increasingly vulnerable to customers using third parties, or going off maintenance and support entirely.

Finding: Despite - of perhaps because of - their dissatisfaction with the current applications support, Oracle Applications customers are not planning a rapid migration to Oracle Fusion Applications, with 5% planning to migrate away from Oracle, 24% researching or planning to migrate to Fusion, and the remainder with no plans to migrate to Fusion. e-Business Suite has the largest percentage of customers considering Fusion Applications, and JD Edwards has the largest percentage of customers considering moving away from Oracle.

My thoughts: Oracle is just beginning to roll out information about Fusion Applications, with the first big "reveal" coming at this year's Oracle Open World. Many Oracle Applications customers have only a limited understanding of the benefits and features, and limitations, of Fusion Applications. Over time, you can expect this result to change dramatically.

Finding: The report includes information about the staff required to run various Oracle Applications products, including e-Business Suite, JD Edwards, Peoplesoft, and Siebel. JD Edwards requires the smallest number of support staff, with e-Bueinss Suite and Peoplesoft at the other end of the spectrum to operate.

My thoughts: There is significant value in this section, and in the report recommendations, for Oracle Applications customers.

Computer Research has done the industry another mitzvah in sponsoring and executing this research and analysis project. Oracle Applications customers, and #EnSW vendors, would benefit from reading this insightful report.

After about a week of voting, readers of this blog have identified the companies they believe Oracle will acquire next. I'll leave the survey open for a while longer, but about 250 people have voted and the results are pretty clear.

Informatica

Overwhelmingly, respondents to this survey believe that Informatica is the company Oracle is most likely to acquire soon. Informatica describes itself this way:

Informatica enables organizations to gain a competitive advantage in today’s global information economy by empowering them to access, integrate and trust all their information assets.

That is to say, Informatica helps companies consolidate and make sense of their data. Informatica is well-known for its Extraction, Transformation, and Loading (ETL) tools, but they've expanded their product portfolio and grown their business over the past several years under the remarkable leadership of Oracle alumSohaib Abbasi. Plenty of Informatica's senior executives and employees have worked at Oracle in the past, and the company's headquarters are even located very close to Oracle in Redwood City.

An acquisition of Informatica could fill a very important hole in Oracle's product line, enabling Oracle to consolidate its position in data warehousing and analytics, one of the hottest growth areas in the database market today. Of course, such a deal would have to pass regulatory approval, and there could certainly be antitrust concerns, but I suspect this deal would get some scrutiny before a quick approval.

Salesforce.com

Salesforce.com, the leading independent CRM company and a leading Cloud platform, is our respondents' second choice for a company Oracle is likely to acquire soon. Salesforce.com is also led by an Oracle alum with a great track record: the inimitable and charismatic Marc Benioff. Marc and his team have played a key role in promoting a major architectural shift, and business model shift, in the IT industry, from "on prem" to SaaS and Cloud. Marc, and many of his team are also Oracle alums, which could help with the integration in a merger with Oracle.

Unfortunately, I think this acquisition is not likely to occur. Salesforce.com is currently valued at about $15 billion, and an acquisition would likely drive this price up to at least $18 billion. It's hard to see how Oracle could make the financials of this deal work. This deal would also likely generate more regulatory scrutiny than an deal for Informatica, but I think this would also get approved under the same theory that led to approval of the acquisitions of Siebel and Peoplesoft.

The Top 10

Of the companies our survey respondents think Oracle will acquire next, most are platform technology companies:

Company

Responses

Informatica

66

Salesforce.com

36

VMware

30

TIBCO

27

Red Hat

26

Teradata

26

NetSuite

25

SuccessFactors

19

Taleo

19

Computer Associates

17

Salesforce.com, NetSuite, SuccessFactors, and Taleo are the applications companies that made the "Top 10" list. What do they have in common? Each is a SaaS application. Salesforce.com is a SaaS CRM company (with a growing Cloud platform (PaaS) business); NetSuite is a SaaS ERP suite (with a growing PaaS business); SuccessFactors and Taleo are SaaS human resources businesses. Acquiring any of these companies is likely to help accelerate Oracle's entry into the SaaS business.

The Write-Ins

In addition to the votes for companies named in the survey, respondents were given the option to write in a choice of their own. 18 responses were written in, a fairly high rate (almost 10% of respondents wrote in another choice).

5 of the write-in "ballots" were for Cloudera, the Hadoop company. Hadoop is a leading technology in the area of "Big Data," a topic that has to be on Oracle's mind as it considers opportunities and threats in the future.

There were a couple of write-in votes each for Vertica and Jive Software. Vertica is the latest start-up from database legend Michael Stonebraker, creator of Ingres, Postgres, and other technically interesting database companies. Vertica's main product is its columnar database, a technology that could be interesting for certain data management problems (like data warehousing). Jive Software is social software for the enterprise, which could help Oracle build next-generation applications.

Best Answer

The best write-in answer was provided by an anonymous survey respondent whose answer to "Who will Oracle acquire next?" was both funny and prescient. The response, given the day before the official announcement: Mark Hurd.

Oracle Alums

I ran the same survey among a group of relative insiders, the OracAlumni Network. This is a group of 500o+ former Oracle employees, many of whom remain in close contact with Oracle and its market, and who believe that Oracle will acquire next:

Informatica Salesforce.com VMware NetSuite Red Hat TIBCO SuccessFactors EMC Symantec Teradata

Very similar list, particularly at the top end.

Summary

If our survey respondents are any indication, Oracle will continue acquiring companies, and Informatica should be at the top of its shopping list. If you'd like to chime in with your thoughts, visit our continuing survey at http://polldaddy.com/poll/3714778/.

I would have put Industry Solutions at the left, to show a real spectrum from industry to application to middleware to database to hardware, but this graphic reveals real insight into Oracle's strategy and focus on acquisitions over the past 5 years.The article also points out some interesting analysis of what characterizes a good deal for Oracle. According to Stephen:

At the highest level, the motivations behind Oracle’s largest acquisitions appear to be the following:

Grow market share leadership in key enterprise markets;

Expand profitability by consolidating high-margin support revenue; and,

Increase strategic relevance by offering a complete technology stack.

This last bullet is something that has played a larger role in really only two of Oracle's acquisitions, both recent, but does two points define a trend? It certainly makes sense and is consistent with speaking points from the company's senior executives.

Today, I got an alert from Java that an update was available, so I clicked "OK" to install. Imagine my surprise when I got the following prompt during the installation procedure:

Is Larry Ellison aware that Oracle (which now owns Sun and its Java products) is promoting Microsoft Bing? By the way, a colleague told me that he received a similar promotion for a Yahoo! toolbar rather than the Bing toolbar, so perhaps Oracle is not solely promoting Microsoft, and perhaps this deal was done before the acquisition. Still, it's odd that Oracle would promote a Microsoft product.

It's even odder that Microsoft is so anxious to promote Bing that it will even do so while subsidizing Java and paying Oracle, two that must be high on Microsoft's "Most Wanted" hit list - does Steve Ballmer know that Microsoft is paying money to Oracle, and (horror of horrors!) subsidizing Java???

Last week, I shared some advice for CEO's as gleaned from colleagues at Enterprise Irregulars. A few more chimed in this week, and I thought I'd share some more advice to enterprise software industry CEO's.

Greg Gianforte

Fix your messaging finally. It's been a problem way too long. Everything else is getting to be so right.

John Chambers

Get serious about SaaS. It sells more routers.

Explain to us again why you are going after HP's far lower margin server business and pissing a bull off which is 3 times your size?

Larry Ellison

Give it up on the cloud already. You know you need it and so many of your execs and customers love it.

Be a better partner or be ganged up on.

Leo Apotheker

Choose your co-CEO now.

Get your message straight. You're not an "in memory, end to end process, SaaS and Cloud hybrid model committed, whatever else you think you are" company. You're an enterprise solutions provider with more innovation than you ever let on. Let people know that. There's nothing to be ashamed of and its still "hip."

Marc Benioff

Love you, keep up the innovation, but stop interrupting your partners and customers onstage. Looks REALLY bad. AND show up ontime to your keynotes. The attendees' time is valuable too. Plus Service Cloud 2, Sales Cloud 2, Custom Cloud 2 and Chatter aren't 4 "clouds." Finally, please, keep growing your philanthropy. That's our view into your real heart - and it does SO much good for so many.

Mark Hurd

Time to leave. You're killing HP.

Randall Stephenson

The Fake Steve Jobs only threatened. The real Steve Jobs will fly over and smash your face with a rock if you keep trying to "incentize" iPhone customers to use less of your network.

Sam Palmisano

AARP will honor you this year for being most committed to technology elders. Your data centers, Lotus, Tivoli and other software portfolio, and your average SAP consultant all are the oldest in the business.

Steve Ballmer

I don't know what to make of you or your company anymore. That's not a good thing. Figure out what it takes to get your customers and folks like us to make SOMETHING of you.

Zach Nelson

Keep fixing customer service. Lay off the stupid anti-SAP campaign. Its neither clever, cute, nor wins you anything. You've got a good thing going with your product now. Get in alignment with that. Keep integrating social features as you are doing now. Way to go.

More great advice there from some really smart, experienced people. If you have any to add, just put in your comment below or at http://dbmoore.blogspot.com/. Thanks!

I feel very honored to be a member of the Enterprise Irregulars group - a very plugged group of people, with lots of hands-on knowledge and experience. I asked them what advice they'd like to give to enterprise solutions company CEO's, and I got the following fascinating list of suggestions.

Carol Bartz

Ya gotta know when to fold 'em, sometimes even the best poker players come up with a deuce/three offsuit.

Dave Duffield

Keep control. No more "got the moves" CEOs.

Eric Schmidt

Don't lose your newfound cash flow and cost cutting religion just because the needle is moving up and to the right again.

Enjoy. Really. Cut some costs if you can. Its all good.

Experiments are fun, but you are a one trick pony and don't have the same power to monopolize that market the way Microsoft did. Ad-supported revenue will die, so cannibalize yourself and diversify with meaningful revenue streams before someone else does it for you.

Jeff Bezos

Have a chat with Larry & Bill. See who wants to find the next greatest CEO for their company. Spin out retail under Zappos guy or someone else. And go be a computer industry God by continuing to simultaneously kick some serious butt - you are the only one who can take on Google (see Google Products & Checkout) and Apple (see music/books/devices) and stand your ground.

Keep on keepin on, no one does it better.

Love what you're doing with cloud computing, but 2010 might be the year to spin it off and let it go its own way.

John Chambers

Pay a dividend, recognize you're an awesome cash flow machine that's only going to grow via acquisitions.

You got game - keep delivering on Telepresence and revolutionalize the data center.

Karl and Pam Lopker

Talk to Vivek and follow the same advice.

Larry Ellison

IBM's multi-billion dollar mainframe business is ripe for the plucking with some juicy margins. Sell non-core Sun businesses, and do your magic. Your stock will be $30 before end of next year.

There's blood in the water, don't let up and keep pressing.

Your consolidation call was timely, and unbelievably effectively done, but 2010 is the year to take Oracle back to a path of innovation. Stop focusing so much on cost-cutting, and unleash some entrepreneurialism within Oracle to drive it to a $300B market cap.

Lars Dalgaard

While you still can, and the Street hasn't figured you out, use your ridiculously lofty valuation and goodwill to acquire the technology edge you don't have but many think you do.

Leo Apotheker

Take solace in the fact you got a chance to be CEO, most don't.

SAP could be a platform for business efficiency - think about providing services that are not software-oriented in 2010. How about doing (across multiple SAP customers) supplier scoring, credit rating, and other benchmarking offerings?

Marc Benioff

Religion only takes you so far, sell to Oracle now while you can.

Keep it up - you're doing great!

Mark Hurd

Call it a career, before HP starts trying to win (and fails) against the big boys. Oracle still has the valuation and capital to make it happen.

Sam Palmisano

Buy SAP while people still think it's a premium asset.

Steve Ballmer

Hire Jeff Bezos as your replacement by acquiring AWS for a ridiculous sum.

Keep up your fiscal discipline, break the company apart, and DON'T go acquisition crazy

Time to retire.

Steve Jobs

Keep those doctors on retainer, at least until the tablet revolutionizes home entertainment a la the iPhone has done with mobile computing.

Steve Singh

Keep it up, you've got the magic and don't need to sell.and don't be afraid of an aggressive acquisition spree.

Vivek Randive

If you get a legit offer, don't be too proud, sell and move on.

Zach Nelson

The sooner you're honest with yourself about what your company is and can be, the sooner the market will treat you with a modicum of respect.

Lots of great advice there from some really smart, experienced people. If you have any to add, just put in your comment below or at http://dbmoore.blogspot.com/. Thanks!

Apparently, the EU is concerned about the possible anti-competitive potential of the Oracle acquisition of mySQL as part of Oracle's purchase of Sun. I contacted the EU, and they forwarded me a survey they are sending to Oracle's competitors who may be affected by the acquisition. There is a second survey they sent me for those who consider themselves to be customers who may be affected by the acquisition. For those who want to comment on the acquisition, the surveys may be obtained by contacting "Adrian.LUEBBERT@ec.europa.eu", and the surveys must be filled out and returned by August 13, 2009 (presumably Close of Business during CET).

Reading the surveys, I am struck by how naive or nefarious the author of the survey was. The questions are phrased in such a way as to justify action to prevent the acquisition from approval by the EU anti-trust regulators. For example:

In your view, do all database products compete with each other? Yes No

No room for "To some very limited extent." Or:

To your knowledge, are there any operating systems which would support exclusively databases offered by the same company as the company offering the respective operating system? For example, are there any operating systems of IBM or Microsoft that would only support IBM databases of Microsoft databases respectively?

How about "Are there any databases that run only on the maker's operating system?"

In any case, here are the two surveys for your own perusal. The first is the survey sent to competing vendors, and the second to customers who may be affected.

Vendor survey

I. INTRODUCTION

On 30 July 2009, Oracle Corporation (hereafter named “Oracle”) notified to the European Commission under the Merger Regulation (Council Regulation (EC) No 139/2004), their intention to acquire SUN Microsystems Inc. (hereafter named "Sun"; both Oracle and Sun will be named hereafter "the parties").

Under the Merger Regulation, the Commission has to assess the proposed transaction's impact on competition. To that end, it must examine in an in depth manner the structure of the markets in which the activities of the above‑mentioned companies overlap or are related to each other. It must gather data on the subject from the parties, but also from other market players, in particular customers and competitors.

Your detailed reply to the questionnaire is very important for us in examining the notified transaction. We would be grateful for any additional remarks you may wish to make concerning the potential impact of the proposed transaction on competition. Please feel free to send us any documentation, studies, articles, etc. on the relevant markets, which in your view may help us in our analysis. If you consider any of the questions irrelevant, please say so and give your reasons.

Please reply for all the companies in your group. With respect to financial data, please give the figures for 2008 (alternatively 2007 if no figures exist yet for 2008) and express monetary amounts, unless requested otherwise, in thousands of Euro.

All information which is clearly marked “confidential” will be treated as such[1].You are kindly requested to provide a non-confidential version of your reply.

The Commission is aware that answering the questionnaire may involve a considerable amount of work.We thank you in advance for your assistance and co-operation. If you have questions about the questionnaire, please contact any of the case handlers:

If you have any general queries or if you would like to receive the electronic copy of this questionnaire, please contact the case secretariat:

- Ms Marianna CSEH (phone: +32-2-298.42.37; marianna.cseh@ec.europa.eu).

We would encourage you to complete the questionnaire in electronic form. If you so decide, please send an e-mail with the following text in the subject line of the e-mail “Case COMP/M.5529 Oracle/Sun ‑ Request Q-Comp Databases in e-format” to the case secretariat from which you will receive the electronic copy. If you so request, you will receive a confirmation of receipt of your submission.

Please return your reply at the latest by 13 August 2009.

II. GENERAL DETAILS

1.Please give the contact details of the person we can contact in case we have questions on your reply:

Company:

Contact person:

Phone:

Position

Fax:

Address:

Country:

Company web-site:

2.Please give a brief description of your company's business in the field of databases, including in particular, the products and services sold by your company in this field.

3.Please indicate your net turnover in 2008 (or 2007 if not available for 2008 yet) in million EUR achieved world-wide and in the EEA[2] (i.e. total sales after deduction of value added tax).

II. QUESTIONNAIRE

A.Market definition

Relevant product market

In order to examine the competitive effects of the proposed transaction on the market, the Commission is required to define the “relevant product markets”. A relevant product market comprises all those products and/or services which are regarded as interchangeable or substitutable by the customers, by reason of the products’ characteristics, prices and intended use.

Oracle's and Sun's activities overlap in database products, more precisely in relational database management systems. Databases are software programmes designed to organise, store, analyse and retrieve information.

4.Please list your product offerings in the field of databases. By ticking the appropriate boxes, please also specify for each of your database products whether the product is proprietary or "open source", whether they can be deployed on Unix-based operating systems, Linux/Open Source Systems, Windows NT or other operating systems.

Proprietary v. Open Source

Operating system

Product

Proprietary

Open Source

Unix

Linux

Windows NT

Other

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

¨

5.Please list the most important characteristics of your respective databases (technical characteristics, efficiency, cost, suitability for any specific application, etc) that lead your customers to purchase these databases.

6.Please indicate whether there are technical or practical barriers to switching between databases.

7.Please indicate whether you provide technical support for:

9.Please provide your view on the way customers take purchasing decisions for databases. Which of the following statements is the most appropriate?

¨Database customers usually decide to purchase databases that best meet their needs AND are compatible with their existing server infrastructure and server operating system; or

¨Database customers usually decide to purchase those databases that best meet their needs AND THEN adapt their server and server operating system to the newly purchased database if necessary; or

¨Database customers usually take purchase decision about server, server operating system and database at the same moment; or

¨Other (please specify)

10.To your knowledge, are there any operating systems which would support exclusively databases offered by the same company as the company offering the respective operating system? For example, are there any operating systems of IBM or Microsoft that would only support IBM databases of Microsoft databases respectively?

11.In your view, is the choice of a database product dictated by the operating system(s) in use in a company? Are there databases that a company could not consider as substitutes because the operating systems in use in the company would limit the choice? Please elaborate.

12.Do customers use databases from different suppliers alongside each other, in particular proprietary databases alongside open source databases? Please elaborate.

13.If you offer open source databases, do you generate revenues from these databases? If yes, please explain the way you generate revenues (commercial licenses, support services etc.).

14.In your view, do all database products compete with each other?

YesNo

Please give reasons for your answer.

15.If you are of the view that only certain database products compete with each other, specify how you would delineate categories of database products that compete with each other and give reasons.

16.In your view, do open source database products and proprietary database products compete with each other?

YesNo

Please give reasons for your answer. If your answer is yes, please specify for which uses open source database products and proprietary database products compete. Please specify also which proportion of your sales of databases competes, i.e. which proportion of your sales of proprietary databases competes with open source databases and which proportion of your open source databases competes with proprietary databases.

Relevant geographic market

A relevant geographic market comprises the area in which the conditions of competition are sufficiently homogenous and which can be distinguished from neighbouring geographic areas because, in particular, the conditions of competition are appreciably different in those areas.

17.Do you see any reason why the geographical dimension of the market for databases should be less than worldwide? Please explain.

18.When selling a database, are there any geographical restrictions on the database license? Are prices different from one country/region to the other?

B.Market data

19.Please provide information on your revenues in 2008 in EUR '000 for your database products. Please distinguish between revenues from licenses and from service or support contracts. Please distinguish as well between proprietary and open source database products.

PROPRIETARY DATABASES

TURNOVER for 2008

(in EUR '000)

EEA

Worldwide

New licenses

Service

New licenses

Service

OPEN SOURCE DATABASES

TURNOVER for 2008

(in EUR '000)

EEA

Worldwide

New licenses

Service

New licenses

Service

20.Please provide information on your units sold of your database products in 2008. Please distinguish between proprietary and open source database products.

PROPRIETARY DATABASES

Units sold in 2008

EEA

Worldwide

OPEN SOURCE DATABASES

TURNOVER for 2008

(in EUR '000)

EEA

Worldwide

C. Competitive assessment

Competitors

21.In the context of tender processes and the conclusion of commercial agreements, which databases do you usually face as competitors? Which databases do you consider as being close competitors to your offering (please list the competitor for each of your product and indicate whether their products are proprietary or open source)? Please list the competitors form the closest competitor to the more distant.

22.Please – to your best knowledge – list Oracle's main competitors in the database market, including yourself. Please indicate whether there are different characteristics/abilities between these competitors. Please rate for each company from 1= "closest" to 10= "less closely" the intensity of competition) and give reasons for this rating. Please specify in which geographic area these competitors are active (e.g. worldwide, EEA, national markets).

Company

Characteristics and abilities

Intensity of competition

Reasons for rating

Geographic area

23.Please – to your best knowledge – list Sun's (MySQL) main competitors in the database market, including yourself. Please indicate whether there are different characteristics/abilities between these competitors. Please rate for each company from 1= "closest" to 10= "less closely" the intensity of competition) and give reasons for this rating. Please specify in which geographic area these competitors are active (e.g. worldwide, EEA, national markets).

Company

Characteristics and abilities

Intensity of competition

Reasons for rating

Geographic area

24.Do you consider that Oracle's database offerings, in particular its database 11g, and Sun's MySQL database offerings constitute direct substitutes from a customer's perspective (taking into account in particular pricing and functionality), and that they would act as direct competitors on the market? Please elaborate.

25.Do you consider that the Oracle database 11g Express Edition constitutes a substitute to MySQL? Please reason your view.

26.Do you consider that the Oracle database 11g Standard Edition constitutes a substitute to MySQL? Please reason your view.

27.Do you consider that the Berkeley DB constitutes a substitute to MySQL? Please reason your view.

28.It has been stated that MySQL is rather complementary to Oracle's database offerings than competing with Oracle's databases. Do you agree? Please reason your view.

29.If you are a company providing technical support for MySQL, in your opinion, what will be the impact of the transaction on your possibilities to provide technical support? Do you expect that you will be able to continue to provide technical support for MySQL if the proposed transaction is implemented? Under which conditions would it be impossible for you to continue to provide technical support? Are you in any contractual relationship with Sun for providing technical support for MySQL? If yes, could you please indicate the terms (e.g. length)?

30.Please indicate whether there are new entrants in the database market that may grow into future strong competitors (in particular open source offerings).

"Forking"

31.Please explain the process of "forking" MySQL with a view to entering the database market, especially as regards:

a)existing technical, legal and other obstacles, in particular relating to the MySQL trademark,

b)additional technical, legal and other obstacles Sun could pose to prevent a "forked" version from entering the market, in particular relating to Sun's partner agreements

c)the costs incurred upon an unsuccessful attempt to enter the market,

d)the time consumed by developing a "fork" and successfully entering the market.

32.In your view, would Oracle, as a result of the proposed transaction, have the ability to prevent forks of MySQL from being developed and from entering the database market?

33.It has been stated that the open source nature of MySQL eliminates potential for anti-competitive effects. Do you agree with this statement? Please reason your view.

34.In your opinion, how important is it for a company offering open source databases to also have the ability to issue commercial licenses, i.e. to apply the dual licensing approach chosen by Sun for MySQL? What are the advantages of such an approach?

35.Do you consider that offerings like Maria DB have the potential to grow as competitive force in the market for databases? Would such growth be accelerated if Oracle failed to continue developing MySQL or if it stopped the MySQL open source offering?

Future development of MySQL

36.Absent the transaction, how would you expect Sun to develop MySQL in comparison to Oracle's database products? Please elaborate.

37.Absent the transaction, how would you expect the competitive relationship between Oracle and Sun as regards database offerings to change in the next 3-5 years? Please elaborate, especially as regards pricing and functionality.

38.In your view, has Oracle's acquisition of Berkeley DB lead to:

¨Improvement of the product;

¨No change of the product;

¨Degradation of the product.

Migration of customers

39.To the best of your knowledge, will Oracle, as a result of the proposed transaction, be in a position to lock in customers of MySQL to Oracle's offering by directing MySQL customers wishing to switch to other databases towards Oracle's proprietary database offerings? Which would be the mechanisms that Oracle could use to direct customers wishing to switch? Are you also able to offer support services to MySQL that would direct customers wishing to switch to certain specific proprietary databases by facilitating the switching?

40.Please also elaborate on how a strategy to "lock in" customers would affect Oracle's/Sun's profits, your database software business and the pricing of database software and related maintenance services.

Vertical aspects

41.To the best of your knowledge, do you consider that Oracle, as a result of the proposed transaction, would be capable of modifying the operating system "Solaris" in a way that degrades its interoperability with database software other than Oracle's or Sun's?

42.Please also elaborate on how such changes to Solaris would affect Oracle's/Sun's profits, your database software business and the pricing of database software and related maintenance services.

D.Conclusion

43.Please describe in detail ALL possible effects and impacts of the proposed transaction on competition in the database market (segment) concerning e.g.:

a)your business

b)your product offerings

c)prices of your and other product offerings

d)product innovation

e)any other parameter?

Please give reasons for your answer.

44.Please provide any other comments that you may have on the proposed transaction.

***

Please remember to provide a non-confidential version of your reply!

THANK YOU VERY MUCH FOR YOUR ASSISTANCE!

[1]Cf. Article 17 of Commission Regulation (EC) No 447/98 of 1 March 1998.

[2]The EEA comprises the 27 Member States forming the European Union and the EFTA countries Iceland, Liechtenstein and Norway.

Customer survey

I. INTRODUCTION

On 30 July 2009, Oracle Corporation (hereafter named “Oracle”) notified to the European Commission under the Merger Regulation (Council Regulation (EC) No 139/2004), their intention to acquire SUN Microsystems Inc. (hereafter named "Sun"; both Oracle and Sun will be named hereafter "the parties").

Under the Merger Regulation, the Commission has to assess the proposed transaction's impact on competition. To that end, it must examine in an in depth manner the structure of the markets in which the activities of the above‑mentioned companies overlap or are related to each other. It must gather data on the subject from the parties, but also from other market players, in particular customers and competitors.

Your detailed reply to the questionnaire is very important for us in examining the notified transaction. We would be grateful for any additional remarks you may wish to make concerning the potential impact of the proposed transaction on competition. Please feel free to send us any documentation, studies, articles, etc. on the relevant markets, which in your view may help us in our analysis. If you consider any of the questions irrelevant, please say so and give your reasons.

Please reply for all the companies in your group. With respect to financial data, please give the figures for 2008 (alternatively 2007 if no figures exist yet for 2008) and express monetary amounts, unless requested otherwise, in thousands of Euro.

All information which is clearly marked “confidential” will be treated as such[1].You are kindly requested to provide a non-confidential version of your reply.

The Commission is aware that answering the questionnaire may involve a considerable amount of work.We thank you in advance for your assistance and co-operation. If you have questions about the questionnaire, please contact any of the case handlers:

If you have any general queries or if you would like to receive the electronic copy of this questionnaire, please contact the case secretariat:

- Ms Marianna CSEH (phone: +32-2-298.42.37; marianna.cseh@ec.europa.eu).

We would encourage you to complete the questionnaire in electronic form. If you so decide, please send an e-mail with the following text in the subject line of the e-mail “Case COMP/M.5529 Oracle/Sun ‑ Request Q-cust Databases in e-format” to the case secretariat from which you will receive the electronic copy. If you so request, you will receive a confirmation of receipt of your submission.

Please return your reply at the latest by 13 August 2009.

II. GENERAL DETAILS

1.Please give the contact details of the person we can contact in case we have questions on your reply:

Company:

Contact person:

Phone:

Position

Fax:

Address:

Country:

Company web-site:

2.Please give a brief description of your company's business, including in particular, the products and services sold by your company.

3.Please indicate your net turnover in 2008 (or 2007 if not available for 2008 yet) in million EUR achieved world-wide and in the EEA[2] (i.e. total sales after deduction of value added tax).

III. QUESTIONNAIRE

A.Market definition

Relevant product market

In order to examine the competitive effects of the proposed transaction on the market, the Commission is required to define the “relevant product markets”. A relevant product market comprises all those products and/or services which are regarded as interchangeable or substitutable by the customers, by reason of the products’ characteristics, prices and intended use.

Oracle's and Sun's activities overlap in database products, more precisely in relational database management systems. Databases are software programmes designed to organise, store, analyse and retrieve information.

4.Please list the database products in use by your company in the table below (indicating the name of the database, the name of the supplier, whether it is open-source or proprietary, the name of the company offering support for each database, the date of purchase and the operating system on which the database is running). Please describe the purpose for which your company purchased the database products and the main characteristics of the products (technical characteristics, efficiency, cost, suitability for any specific application, etc).

Database

Supplier

Open-Source (Yes/No)

Support supplier

Date of purchase

Operating System

Purpose and main characteristics

5.Does you company purchase technical support for:

¨MySQL;

¨Other open source databases (please specify).

6.If your answer to the previous question is yes, from which company do you purchase technical support?

7.Do you use databases from different suppliers alongside each other, in particular proprietary databases alongside open source databases? Please elaborate. For which purpose do you use these databases?

8.Please indicate the cost of owning the databases listed above and the support costs associated with them (indicate 2008 payments).

Database

Cost of license in 2008 (€)

Cost of support in 2008 (€)

9.For each of the products listed above, please indicate the competing products that would be suitable for replacing your current database products. Please describe briefly their main characteristics (strengths and weaknesses) and the factors that make the competing products suitable to replace the products you sourced instead.

12.More generally, what are the costs and the difficulties associated with switching databases?

13.How do you take purchasing decisions for databases? Which of the following statements is the most appropriate?

¨Your company decides to purchase databases that best meets its needs AND is compatible with the existing server infrastructure and server operating system; or

¨Your company decides to purchase those databases that best meet its needs AND THEN adapt its server and server operating system to the newly purchased database if necessary; or

¨Your company usually takes purchase decision about server, server operating system and database at the same moment; or

¨Other (please specify)

14.Is the choice of a database product dictated by the operating system(s) in use in your company?Are there databases that you could not consider as substitutes because the operating systems in use in your company limit your choice?

15.In your view, do all database products compete with each other?

YesNo

Please give reasons for your answer.

16.If you are of the view that only certain database products compete with each other, please specify how you would delineate categories of database products that compete with each other and give reasons.

17.In your view, do open source database products and proprietary database products compete with each other?

YesNo

Please give reasons for your answer. If your answer is yes, please specify for which uses open source database products and proprietary database products compete.

Relevant geographic market

A relevant geographic market comprises the area in which the conditions of competition are sufficiently homogenous and which can be distinguished from neighbouring geographic areas because, in particular, the conditions of competition are appreciably different in those areas.

18.Do you see any reason why the geographical dimension of the market for databases should be less than worldwide? Please explain.

19.When selling a database, are there any geographical restrictions on the database license? Are prices different from one country/region to the other?

B. Competitive assessment

Competitors

20.Please indicate by order of importance your five main suppliers for databases.

21.Please – to your best knowledge – list Oracle's main competitors in the database market. Please indicate whether there are different characteristics/abilities between these competitors. Please rate for each company from 1= "closest" to 10= "less closely" the intensity of competition) and give reasons for this rating. Please specify in which geographic area these competitors are active (e.g. worldwide, EEA, national markets).

Company

Characteristics and abilities

Intensity of competition

Reasons for rating

Geographic area

22.Please – to your best knowledge – list Sun's (MySQL) main competitors in the database market. Please indicate whether there are different characteristics/abilities between these competitors. Please rate for each company from 1= "closest" to 10= "less closely" the intensity of competition) and give reasons for this rating. Please specify in which geographic area these competitors are active (e.g. worldwide, EEA, national markets).

Company

Characteristics and abilities

Intensity of competition

Reasons for rating

Geographic area

23.For each of the databases in use in your company (as listed in question 4), at the time your company made the purchasing decision, please indicate in the table below which other competing databases you were also considering purchasing.Please indicate the reasons why you chose the database you are currently using.

Database in use

Competing databases considered at the time of purchase

Reasons for the choice

24.Do you consider that Oracle's database offerings, in particular its database 11g, and Sun's MySQL database offerings constitute direct substitutes (taking into account in particular pricing and functionality), and that they act as direct competitors on the market? Please elaborate.

25.It has been stated that MySQL is rather complementary to Oracle's database offerings than competing with Oracle's databases (i.e. in the sense that MySQL and Oracle targets different needs). Do you agree? Please reason your view.

26.Do you or would you use Oracle databases and Sun databases side by side for similar tasks? Please elaborate.

27.Do you or would you use Oracle databases and Sun databases side by side in your company for different tasks? Please elaborate.

28.Do you have plans to change your database products? If yes, please elaborate what are the reasons for the change.

29.If your company purchases technical support for MySQL from Sun and in case Oracle, after the transaction, increased prices for technical support of MySQL, would you be prepared to switch to another company providing such technical support services? If yes, to which company would you be most likely to switch?

30.If your company purchases technical support for MySQL from a company other than Sun, in your opinion, what will be the impact of the transaction on your possibilities to purchase technical support from a company other than Oracle? Do you expect that you will be able to continue?

31.Please indicate whether there are new entrants in the database market that may grow into future strong competitors to the current suppliers (in particular open source offerings).

Commercial MySQL license

32.Have you purchased a commercial MySQL licence? If yes, please describe the purpose for which your company purchased the commercial license. Why would a GNU General Public License v.2 not be sufficient for your purposes?

33.Please indicate the duration of your company's contract for the commercial MySQL license.

34.Could your company replace the commercial MySQL license by another commercial database license available on the market?

35.What would be the impact on your company if a commercial MySQL license would not be available anymore?

"Forking"

36.Please explain the process of "forking" MySQL with a view to entering the database market, especially as regards:

a)existing technical, legal and other obstacles, in particular relating to the MySQL trademark,

b)additional technical, legal and other obstacles Sun could pose to prevent a "forked" version from entering the market, in particular relating to Sun's partner agreements

c)the costs incurred upon an unsuccessful attempt to enter the market,

d)the time consumed by developing a "fork" and successfully entering the market.

37.In your view, would Oracle, as a result of the proposed transaction, have the ability to prevent forks of MySQL from being developed and from entering the database market?

38.It has been stated that the open source nature of MySQL eliminates potential for anti-competitive effects. Do you agree with this statement? Please reason your view.

39.In your opinion, how important is it for a company offering open source databases to also have the ability to issue commercial licenses, i.e. to apply the dual licensing approach chosen by Sun for MySQL? What are the advantages of such an approach?

40.Do you consider that offerings like Maria DB have the potential to grow as competitive force in the market for databases? Would such growth be accelerated if Oracle failed to continue developing MySQL or if it stopped the MySQL open source offering? In particular, would your company consider using Maria DB?

Future development of MySQL

41.Absent the transaction, how would you expect Sun to develop MySQL in comparison to Oracle's database products? Please elaborate.

42.Absent the transaction, how would you expect the competitive relationship between Oracle and Sun as regards database offerings to change in the next 3-5 years? Please elaborate, especially as regards pricing and functionality.

43.Does your company purchase any open source products from Oracle? If yes, how do you assess Oracle's support for and commitment to this open source product?

44.In your view, has Oracle's acquisition of Berkeley DB lead to:

¨Improvement of the product;

¨No change of the product;

¨Degradation of the product.

Migration of customers

45.To the best of your knowledge, will Oracle, as a result of the proposed transaction, be in a position to lock in customers of MySQL to Oracle's offering by directing MySQL customers wishing to switch to other databases towards Oracle's proprietary database offerings? Which would be the mechanisms that Oracle could use to direct customers wishing to switch?

46.Please also elaborate on how a strategy to "lock in" customers would affect Oracle's/Sun's profits, your database software business and the pricing of database software and related maintenance services.

Vertical aspects

47.To the best of your knowledge, do you consider that Oracle, as a result of the proposed transaction, would be capable of modifying the operating system "Solaris" in a way that degrades its interoperability with database software other than Oracle's or Sun's?

48.Please also elaborate on how such changes to Solaris would affect Oracle's/Sun's profits, your database software business and the pricing of database software and related maintenance services.

49.If Oracle purchases Sun, the newly formed company will have the possibility to offer to its customers a fully integrated stack, from hardware to middleware and enterprise application software, and including operating systems and databases. Please indicate whether you consider that Oracle/Sun will be in a position to foreclose its competitors in the different layers of the stack thanks to this characteristic. What impact could such vertical integration have for customers?

D.Conclusion

50.Please describe in detail ALL possible effects and impacts of the proposed transaction on competition in the database market (segment) concerning e.g.:

a)your business

b)prices for database products

c)product innovation

d)any other parameter?

Please give reasons for your answer.

51.Please provide any other comments that you may have on the proposed transaction.

***

Please remember to provide a non-confidential version of your reply!

THANK YOU VERY MUCH FOR YOUR ASSISTANCE!

[1]Cf. Article 17 of Commission Regulation (EC) No 447/98 of 1 March 1998.

[2]The EEA comprises the 27 Member States forming the European Union and the EFTA countries Iceland, Liechtenstein and Norway.

operational systems, transform that data into unified units and schema, cleanse the data of errors and gaps, aggregate the data to support faster queries, and then deploy that data into the enterprise data warehouse for reporting and analytics use. This process generally introduces a lag between when data are entered into the operational system, and when that same data are available in the data warehouse. This lag can be as short as a few minutes, or as long as a month, but is rarely less than an hour. Many enterprises “refresh” their data warehouse nightly (although when is “nightly” in a global enterprise?) or even weekly. One CRM system I used recently had a caveat on its reports, stating that “the data in this report may be 24 hours out of date.” In other words, on the last day of the quarter, a sales manager could not use the system’s reporting capabilities to determine if she had made her quota or still needed to make some more calls. For some applications, this lag time is unavoidable, but eliminating this gap between action and insight should be a goal of every IT organization.

operational systems, transform that data into unified units and schema, cleanse the data of errors and gaps, aggregate the data to support faster queries, and then deploy that data into the enterprise data warehouse for reporting and analytics use. This process generally introduces a lag between when data are entered into the operational system, and when that same data are available in the data warehouse. This lag can be as short as a few minutes, or as long as a month, but is rarely less than an hour. Many enterprises “refresh” their data warehouse nightly (although when is “nightly” in a global enterprise?) or even weekly. One CRM system I used recently had a caveat on its reports, stating that “the data in this report may be 24 hours out of date.” In other words, on the last day of the quarter, a sales manager could not use the system’s reporting capabilities to determine if she had made her quota or still needed to make some more calls. For some applications, this lag time is unavoidable, but eliminating this gap between action and insight should be a goal of every IT organization. ideas come from the consumer world – this trend is known as “the consumerization of IT” (or #CoIT, to insiders on Twitter). Consumer-facing companies (like Apple and Facebook) hear more clearly from their users and customers than Enterprise Software and Solutions companies (#EnSW on Twitter), and so they are often the source of innovation in the IT space. CoIT gives us many ideas about user experience (iPad!), social capabilities (Facebook!), mobility (iPad!), and scaling to massive data volumes (Facebook!). However, the consumer world does not offer us many good examples of real-time integration of operational and analytical data.